What you need to know about the 2026 Wollongong Apartment Report

Buyers have cleared out near-term supply, but the real test is whether thousands of approved apartments can be delivered.

For years, the debate centred on a shortage of approved apartment projects in Wollongong. Now, with thousands of apartments moving through planning reforms, the focus has shifted to a new question: can the industry deliver what’s been promised?

An early-morning crowd packed Hotel TOTTO in Wollongong on Thursday, June 18, for the launch of Colliers’ eighth annual Wollongong Apartment Report.

Prepared by Colliers’ Marcello Babbili and Kristy Sequeira, the report draws on government data, planning data, sales activity, rental market trends and Colliers’ own project-by-project analysis.

This year’s findings paint a picture of a region caught between scarcity and supply.

Here are eight things that stood out from this year’s report.

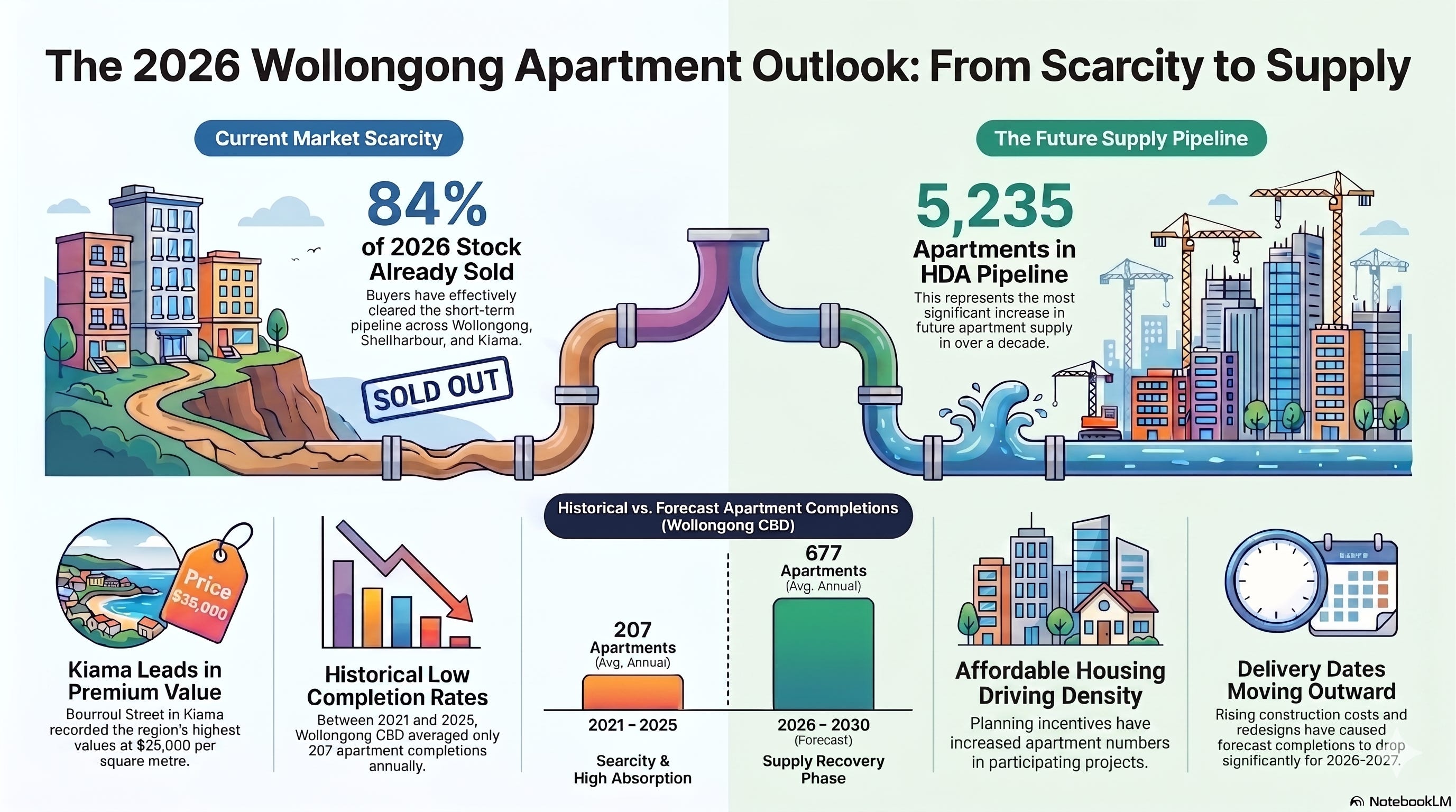

1. Buyers have almost completely cleared out apartments due for completion in 2026

The report found that 84 per cent of apartments due for completion in 2026 across Wollongong, Shellharbour and Kiama have already sold, leaving relatively little stock available for buyers looking to move in the near term.

Colliers Wollongong Managing Director Simon Kersten said buyers had “comprehensively cleared the short-term pipeline”, with the data showing demand continues to absorb new apartments as they approach completion.

“With 84 per cent of 2026 stock already sold, the strategic question is no longer supply — it is delivery,” Mr Kersten said.

2. The next sales race has already started

While apartments due for completion in 2026 are largely sold out, the report found that 29 per cent of apartments forecast for completion in 2027 across Wollongong, Shellharbour and Kiama have been committed.

Mr Kersten said the data pointed to a clear opportunity for developers bringing projects to market in the near term.

“With 2026 effectively sold out and 2027 still under 40 per cent committed, presale velocity can be relied upon for short-term projects. That window remains open, but it is finite,” Mr Kersten said.

3. Wollongong’s 5,000-apartment pipeline comes with a giant asterisk.

One of the headline figures in this year’s report is the emergence of a 5,235-apartment pipeline through the Housing Delivery Authority (HDA) pathway across Wollongong, Shellharbour and Kiama.

Colliers describes the HDA pipeline as the most significant increase in future apartment supply the region has seen in more than a decade.

The report and accompanying presentation suggest the number should be treated with some caution.

Of the 5,235 apartments currently sitting in the HDA process, only 201 apartments have progressed to the exhibition stage, with the overwhelming majority still moving through earlier phases of the planning pathway.

Mr Kersten acknowledged that while the pipeline represents a significant boost to future supply, much of it remains uncertain.

“Whilst there’s a significant amount of apartments in this pipeline, what becomes real will be the question, “ he told attendees.

The report also notes that not all of the 5,235 apartments are genuinely new supply. Many projects were already somewhere within the planning system before entering the HDA pathway.

According to Colliers’ analysis, the HDA has created a net increase of 3,587 apartments, rather than the full 5,235 apartments often referenced in headline figures.

Mr Kersten said developers have six months to progress projects through key stages of the HDA process and revealed some proposals had already fallen out of the system.

“We’re already seeing the department cutting them off if they don’t make the six months,” he said.

4. The pipeline is growing, but the delivery dates keep moving.

The report may point to a record pipeline of future apartments, but it also reveals a growing gap between what has been approved and what is likely to be delivered on time.

Colliers’ updated forecasts show that several projects expected to be completed in 2026 and 2027 have been pushed back. In Wollongong CBD alone, the forecast for 2026 completions has fallen from 840 apartments in last year’s report to 657, while the 2027 forecast has dropped from 643 apartments to 296.

Read what Colliers said in its 2025 Wollongong Apartment Report.

Mr Kersten said planning changes had contributed to some of the delays, with developers redesigning and resubmitting projects through new pathways such as the Housing Delivery Authority and Affordable Housing Scheme.

“We’ve seen two and three delays in some of these projects,” he told attendees.

But planning wasn’t the only challenge.

Mr Kersten said rising construction costs, global uncertainty and weak consumer confidence were also weighing on project feasibility and buyer sentiment.

Later in the presentation, Mr Kersten pointed to the Middle East conflict, cost-of-living pressures and interest rates as factors contributing to market uncertainty, warning that many buyers were becoming increasingly hesitant to commit.

5. Affordable housing is reshaping development feasibility

The report found that planning incentives linked to affordable housing are generating more apartments than would otherwise have been delivered.

The Affordable Housing Scheme has added 984 apartments to participating developments, including 537 affordable homes, by allowing developers to increase density in exchange for providing affordable housing.

Mr Kersten said the affordable housing policy had prompted many developers to redesign and resubmit existing projects, increasing apartment numbers without requiring significant new infrastructure.

“The affordable housing policy has caused a lot of existing DAs in the pipeline to be redrawn and resubmitted, with additional apartments added on,” he said.

“Why is that important? Because we’ve got about 30 per cent more apartments in these projects without any new infrastructure — no new roads, no bulldozing farms. We’ve got 30 per cent more housing on existing sites with very little additional infrastructure required.”

The report found participating developments increased apartment numbers by an average of 28 per cent, making affordable housing incentives one of the most significant sources of additional supply in the region’s pipeline.

6. The Illawarra’s most expensive apartments aren’t in Wollongong

The report found the highest apartment values per square metre in the Illawarra are no longer being achieved in Wollongong.

Instead, Bourrool Street in Kiama recorded the region’s highest apartment values at $25,600 per square metre, followed by Ocean Street, Kiama ($24,192/sqm) and Pitt Avenue, Shell Cove ($22,700/sqm).

7. Rising construction costs are still shaping what gets built

While planning reforms have expanded the apartment pipeline, the report suggests construction costs remain one of the biggest constraints on new development.

Mr Kersten told attendees that feasibility remains a challenge for many projects, despite strong demand for completed apartments.

“We need to look at new construction methods. We need to build a smaller product, we need to build a cheaper product,” Mr Kersten said.

“The current way we’re building things and the current type of stock will never get any cheaper because it costs almost what you sell it for to build it right now.”

He estimated the cost of building a typical two-bedroom apartment in a high-rise project at between $700,000 and $800,000.

8. The scarcity story may only have a few years left

While apartment supply remains constrained in the short term, the report forecasts a significant increase in completions over the coming years.

In Wollongong CBD, apartment completions averaged 207 dwellings a year between 2021 and 2025. The report forecasts that the figure will increase to an average of 677 apartments annually from 2026 onwards.

Mr Kersten said the market’s current supply constraints were unlikely to persist indefinitely as more projects move through the development pipeline.

“We’ve got about two years of that left, maybe three,” he told attendees.

The report’s forecasts suggest the second half of the decade could look markedly different from the first, provided projects currently in the pipeline proceed to construction and completion.

It’s that time of the year: EOFY sale time.

Yes, you can save money with us, too.